GyngerReview: Vendor Financing Rates & Alternatives

If you're reading Gynger reviews or comparing Gynger alternatives, this guide breaks down Gynger's B2B BNPL for software / cloud / GPU purchases, the 3–12 month payment options, the undisclosed APR structure, and the best alternatives for SaaS founders. Founderpath funds the SaaS company directly — so the same cash that pays a vendor bill also covers payroll, growth, and runway, with published starting rates from 7% RPA / 14% APR.

Compared in this guide

Quick Cost Comparison

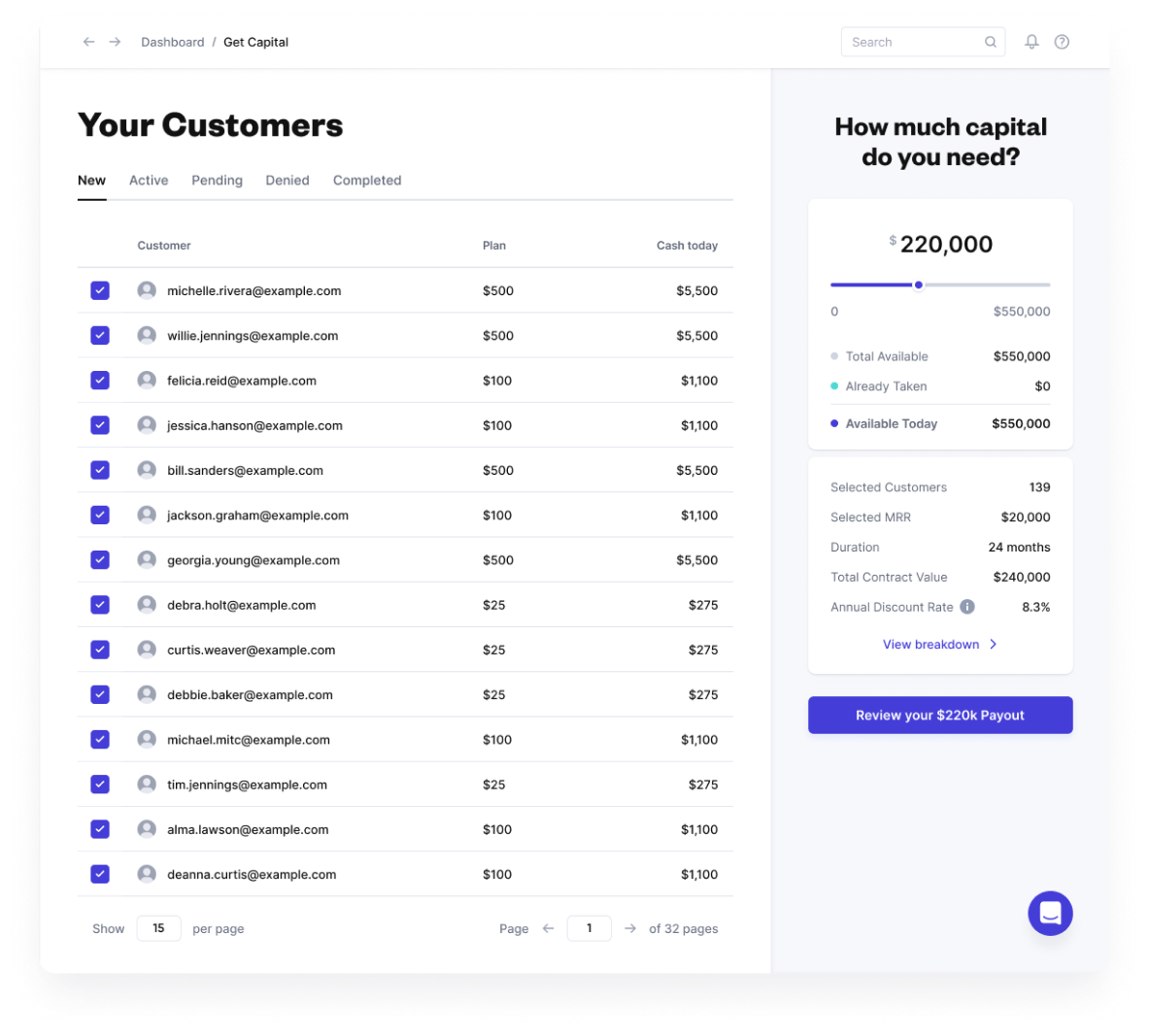

Save $6,032 on total cost vs Founderpath RPA, and cut monthly burden ~$8,733/mo via the Term Loan

Gynger does not publish an APR — adjust to your quote. FP RPA: $17,833/mo over 12mo. FP TL: $9,603/mo over 24mo.

See full breakdown ↓TL;DR

What is Gynger?

Gynger is a New York-headquartered embedded-financing fintech that operates as a B2B buy-now-pay-later (BNPL) platform for technology purchases. Founded in 2021 by Mark Ghermezian (co-founder and founding CEO of Braze, NASDAQ: BRZE) and emerging from stealth in December 2022 with a $21.7M seed round (per the Fintech Global stealth-emergence coverage), Gynger pays a buyer's software / cloud / GPU vendor upfront and the buyer repays Gyngerover 3, 6, 9, or 12 months — or net 30, 60, or 90 for a single balloon payment. The company is HQ'd at 157 W 18th Street, Floor 5, New York, NY.

Gynger's product lineup, per gynger.io and the public FAQ: Bill Financing (Gynger pays a vendor invoice upfront; buyer repays Gynger over the chosen term), Reimbursement Capital (retroactively finance a software bill already paid), Virtual Card(Gynger-issued card “with a lower APR than traditional credit cards” per gynger.io/buyers), AR Financing (vendor-side advance against unpaid customer invoices), and Gynger Pay (embedded checkout widget — vendor gets paid upfront, customer pays Gynger over time). Gynger also markets AP financing for technology payables and has announced direct vendor partnerships including Soluna (renewables-powered high-performance computing) to surface Gynger financing at the vendor's point of sale.

Per the Series A coverage (Fintech Global, June 21, 2024) and Built In NYC, Gynger raised $20M Series A led by PayPal Ventures, alongside a $100M debt facility from Community Investment Management (CIM). Total disclosed capital: approximately $31.7M in equity plus a $110M debt facility stack across both rounds.

Founders compare Gynger alternatives mainly because Gynger finances individual software purchases rather than the SaaS company itself — and because no APR, factor rate, or origination fee is published on gynger.io. Founderpath is the working-capital alternative: instead of spreading a single vendor bill over 12 months, Founderpath funds the SaaS company directly so the same cash pays the vendor bill plus payroll, growth, and runway from one facility. Founderpath offers three capital products with published starting rates: a Merchant Cash Advance (% of monthly sales), a Revenue Purchase Agreement (7% starting flat fee, daily / weekly debits), and a Term Loan (14% APR starting, fixed monthly, up to 48 months).

How Gynger Works

Per the Gynger FAQ, a buyer connects accounting (via Codat) and bank data (via Plaid), submits vendor / contract information, and receives an AI-driven pre-qualification decision in a few minutes. Full approval can happen within 24 hours. Once approved, the buyer chooses a repayment term and signs the in-app Loan Agreement; Gyngerpays the vendor “as soon as the next business day,” and the buyer repays Gynger over the chosen term.

Term options, verbatim from gynger.io/faqs: “net 30, 60, and 90; 3, 6, 9, and 12-month payments.” The longest amortizing term Gynger publishes is 12 months. Net 30 / 60 / 90 are single balloon repayments; the 3 / 6 / 9 / 12-month options amortize monthly.

Pricing is not disclosed publicly. The Gynger homepage, buyer page, product page, and FAQ describe pricing only qualitatively: “low APR virtual card” (gynger.io/buyers), “lower fees than factoring” (gynger.io/faqs, AR Financing). The TechCrunch Series A coverage (June 20, 2024) explicitly describes the revenue model: Gynger“charges interest on its loans and also makes money from buyers on loan origination fees, as well as through interchange fees from its card program… and also generates revenue from vendors via service fees and plans to generate revenue from SaaS/platform fees.” This interest + origination + interchange + vendor-service-fee stack is standard for B2B BNPL lenders, but no specific rate is published.

Gynger does not publish a public Terms of Service, Privacy Policy, or sample Loan Agreement on gynger.io as of May 2026. The financing-specific Loan Agreement is signed inside the Gynger app at the time of each draw — so the contract terms (UCC filings, default provisions, acceleration clauses, prepayment terms) are only visible after the founder has created an account and gone through underwriting. Founders should request a full copy of the Loan Agreement for review before drawing on the facility.

Why Founders Look for Gynger Alternatives

Gynger solves a narrow problem — spreading a single software bill over 3–12 months — and the fact that the buyer never sees the cash is the core structural difference vs Founderpath. Founders comparing alternatives typically want broader use-of-funds, published rates, or longer terms.

- 1.Gynger funds the vendor, not the company.Gynger pays the buyer's software bill upfront; the buyer never sees the cash. That solves cash-flow on a single line item but doesn't help with payroll, headcount, growth experiments, or runway. Founderpath funds the SaaS company directly so the same dollar can do any of those.

- 2.No published rate card.Gynger discloses no APR, factor rate, origination fee, or prepayment penalty on its public site. The marketing language is “low APR” and “lower fees than factoring”; the actual cost only appears in the in-app Loan Agreement. Founderpath publishes starting rates directly: 7% on the RPA, 14% APR on the Term Loan.

- 3.Maximum term is 12 months.Gynger's longest amortizing term is 12 months. On a $200K bill that's ~$18K/month at a typical B2B BNPL APR. Founderpath's Term Loan stretches to 48 months — same $200K at 14% APR over 24 months is ~$9,600/month, roughly half the monthly cash burden.

- 4.One financing relationship per software bill. Gynger draws are tied to a specific vendor invoice — a new Snowflake renewal or AWS contract means a new Gyngerdraw, a new approval, a new payment schedule layered on top of the others. Founderpath is a single facility against the company's ARR; one term sheet covers any business expense, no per-vendor re-approval, no stacked monthly schedules.

- 5.Loan Agreement is not public. Gynger does not publish a Terms of Service, Privacy Policy, or sample Loan Agreement on gynger.io. Contract terms — UCC filings, default and acceleration mechanics, prepayment provisions — are only revealed at the in-app sign-up step, after the founder has invested time in account creation and underwriting. Founderpath shares the Customer Agreement at term-sheet stage.

- 6.No independent review presence. As of May 2026, Gynger does not maintain a profile on Trustpilot, G2, or Capterra. The only public customer feedback is the first-party testimonials on gynger.io/customer-stories. Founderpath holds a 4.9 / 5 rating across 100+ verified Trustpilot reviews from SaaS founders.

- 7.Geographic coverage is undisclosed. Gynger does not state geographic restrictions publicly, but every named customer and vendor on the site is US-based and the integrations (Codat, Plaid) are configured for US banking. Founderpath funds SaaS and ecommerce founders globally — US, Canada, EU, UK, and additional jurisdictions.

Why bootstrapped SaaS founders choose Founderpath— “I'd spent 12 years looking for a fair, transparent debt funding option for my SaaS. The terms are fair, the focus on bootstrapped SaaS founders is unwavering. I feel like I have a financier in my corner.” — Chris Taylor, Canada

Founderpath offers three direct alternatives

Founderpath has three capital products. Pick whichever repayment schedule fits your cash plan — all funded in under 24 hours with published starting rates and global geography:

- →Merchant Cash Advance — for businesses with seasonal cash flows that prefer paying back as a percentage of future monthly sales.

- →Revenue Purchase Agreement (RPA) — from a 7% starting flat discount fee scaling per year, fixed daily or weekly debits, terms up to 36 months. Useful for paying a vendor bill plus extending runway in one move.

- →Term Loan — fixed monthly payments at 14% APR starting, terms up to 48 months (4× the Gynger maximum), no prepayment penalty (save on interest by repaying early).

Founderpath funds SaaS and ecommerce founders globally — including all US markets where Gynger operates plus Canada, EU, UK, and additional jurisdictions — with native integrations to Stripe, Chargebee, and Recurly.

Top 6 Gynger Alternatives

Two categories: working-capital alternatives that fund the SaaS company directly (Founderpath, Lighter, Pipe, Clearco), and B2B BNPL / vendor-financing peers that compete with Gynger Pay (Capchase Pay, Ratio, Slope).

# | Company | Best For | Pricing | Funding Speed |

|---|---|---|---|---|

1 | Founderpath | MCA + RPA + Term Loan — working capital, not just vendor financing | From 7% RPA flat fee or 14% APR Term Loan; MCA % of monthly sales | Under 24 hours |

2 | Capchase Pay (incl. Vartana) | Vendor-side embedded BNPL — CRM-integrated | Not published; ~7%/yr scaling for Capchase Grow | 48 hours |

3 | Ratio | Vendor-side BNPL + true-sale of contracts | Custom; CPQ-integrated | Days |

4 | Slope | B2B BNPL beyond SaaS (goods, services) | Per-deal pricing; not published | Same day |

5 | Settle | AP + working-capital (CPG-leaning) | Per-invoice fee; not published | Days |

6 | Vendr | SaaS procurement / buyer advocacy (not a lender) | Service / subscription fee, no financing spread | Weeks |

Founderpath is the only Gynger alternative on this list that funds the SaaS company directly with capital usable for any purpose — vendor bills, payroll, growth, runway — instead of one specific software bill at a time. Founderpath has funded SaaS and ecommerce founders globally with over $271M in non-dilutive capital across 740+ deals.

Many founders comparing Gynger also evaluate Founderpath vs Clearco and Founderpath vs Lighter Capital.

Pros and Cons of Gynger

Pros

Pays the vendor directly.If the founder's goal is to remove a single vendor invoice from this quarter's cash flow, the structure is clean — Gynger pays the vendor, the buyer never touches the cash.

Pays the vendor directly.If the founder's goal is to remove a single vendor invoice from this quarter's cash flow, the structure is clean — Gynger pays the vendor, the buyer never touches the cash.- Fast underwriting. Pre-qual in minutes; approval as fast as 24 hours; vendor paid the next business day.

- Multiple sub-products. Bill Financing, Reimbursement, Virtual Card, AR Financing, Gynger Pay — covers buyer and vendor sides of the same transaction.

- Vendor partnerships across compute and HPC. Lambda Labs is a supported vendor on the Gynger homepage; Gynger has announced a direct integration with Soluna (renewables-powered HPC) — relevant for founders with large cloud or compute spend.

- Operator pedigree. Founder Mark Ghermezian co-founded Braze (NASDAQ: BRZE); backers include PayPal Ventures, Gradient (Google), Upper90, Vine Ventures.

Cons

Funds the vendor, not the company. No flexibility to use the cash for payroll, growth, or runway — Gynger is locked to vendor invoices.

Funds the vendor, not the company. No flexibility to use the cash for payroll, growth, or runway — Gynger is locked to vendor invoices.- No public rate card. No APR, factor rate, origination fee, prepayment penalty, or late fee disclosed on gynger.io, FAQ, blog, or any product page.

- 12-month max amortizing term.Compresses cash burden vs Founderpath's 24/36/48-month options.

- Per-invoice draws, not a single facility. Each vendor renewal is a separate draw and a separate amortization schedule layered on the previous ones, rather than a single working-capital facility against company ARR.

- No public Terms of Service or sample Loan Agreement. Contract terms only surface in the in-app Loan Agreement at draw time.

- No independent Trustpilot / G2 / Capterra presence. Only first-party testimonials on gynger.io/customer-stories.

- US-only based on public information. No publicly disclosed Canada, EU, UK, or ROW coverage.

What Is the Best Gynger Alternative?

The best Gynger alternative for SaaS founders is Founderpath— because Founderpath funds the SaaS company directly, the same dollar pays the vendor bill AND payroll, growth, and runway from one facility against the company's ARR. Gynger's capital is locked to a specific vendor invoice; Founderpath's is not.

Founderpath's Revenue Purchase Agreement (RPA) starts from a 7% flat discount fee scaling per year, with terms up to 36 months. On a $200K vendor bill at the typical 12-month payback, the FP RPA fee is about $14K (total repayment $214K) — and the cash can pay the vendor bill plus extend runway. The Term Loan starts at 14% APR with fixed monthly payments and terms up to 48 months — four times Gynger's maximum, with roughly half the monthly cash burden. And the Merchant Cash Advance pays back as a percentage of future monthly sales for businesses with seasonal revenue.

Founderpath publishes starting rates on its product pages, shares the Customer Agreement at term-sheet stage, funds in under 24 hours, and serves SaaS founders globally. For founders evaluating vendor-side embedded BNPL specifically (Gynger Pay), Capchase Pay (which absorbed Vartana in June 2025) and Ratio are the closer direct competitors; Founderpath does not offer an embedded vendor-checkout widget.

Gynger Pricing Explained

Gynger does not publish an APR, factor rate, origination fee, prepayment penalty, or late fee on its public site. The homepage, FAQ, buyer page, and product pages describe pricing only qualitatively. Per gynger.io/buyers, the Virtual Card has a “lower APR than traditional credit cards and more flexible terms than standard charge cards.” Per the AR Financing section of the FAQ, the product offers “lower fees than factoring.” Neither sentence quotes a number.

TechCrunch's Series A coverage (June 20, 2024) confirms the revenue model: Gynger “charges interest on its loans and also makes money from buyers on loan origination fees, as well as through interchange fees from its card program… and also generates revenue from vendors via service fees and plans to generate revenue from SaaS/platform fees.” This interest + origination + interchange + vendor-service-fee stack is standard for B2B BNPL lenders, but Gynger has not publicly committed to any specific rate band. Founders should request a written quote with the full all-in APR (including origination + interchange) before drawing.

For modeling purposes, this page assumes a B2B BNPL APR range of 14%–24% — consistent with Gynger's “lower APR than traditional credit cards” marketing language (traditional business credit cards typically run 22%–29% APR per Federal Reserve G.19) and with the published rate bands of comparable B2B BNPL fintechs. This is an estimate, not a Gynger disclosure. Use the calculator below with your actual quote.

By comparison, Founderpath publishes starting rates directly on its product pages. The Revenue Purchase Agreement starts from a 7% flat discount fee scaling per year. The Term Loan starts from 14% APR — fixed monthly, no prepayment penalty, terms up to 48 months. And the Merchant Cash Advance pays back as a percentage of monthly sales for seasonal businesses. No origination fee, no prepayment penalty, no late fee, no personal guarantee, no minimum cash balance covenant.

Is Founderpath Cheaper Than Gynger?

At any plausible B2B BNPL APR on a 12-month amortizing term, yes — Founderpath's RPA is cheaper on total dollar cost. Two caveats: (1) Gynger publishes no rate, so the comparison depends on the actual quote, and (2) the structural difference (vendor bill vs working capital) is usually a bigger deal than the dollar delta.

Scenario: $200,000 vendor bill, 12-month amortizing term (apples-to-apples).

- Gynger Bill Financing at an estimated 18% APR, 12mo amortizing: total ~$220,000, monthly ~$18,300/mo. Cash goes to the vendor, not to the company.

- Founderpath RPA, 12-month term, 7% starting flat fee: total $214,000, monthly ~$17,800/mo — about $6,000 cheaper on total cost. Cash hits the company balance sheet and can pay the same vendor plus payroll, growth, and runway from one facility.

- Founderpath Term Loan, 24-month fixed monthly, 14% APR: total ~$230,000, monthly ~$9,600/mo — total cost higher than the Gynger 12-month deal, but monthly cash burden is roughly half. And the Term Loan saves on interest if you repay early.

Note on annual prepay discounts. Both Gyngerand Founderpath pay the vendor in a single lump sum upfront, so both let the buyer negotiate a typical 10%–20% annual-prepay discount with the vendor (Harbinger's testimonial on gynger.io/customer-stories explicitly references this: “ With Gynger, we were able to pay for high-cost software licenses upfront — unlocking significant discounts from our technology vendors.”) The structural Founderpath advantage isn't prepay-discount access — it's that the same Founderpath dollar is also usable for payroll, hiring, growth experiments, and runway, not locked to one vendor invoice.

Where Gynger's short terms compete. If the buyer picks a 3-month or 6-month Gyngerterm at the low end of the APR range, the total dollar cost can come in under Founderpath's RPA 12mo — because the principal is exposed to interest for less time. The trade-off: monthly cash burden 2×–4× higher and no working-capital flexibility. The calculator below models every combo so you can run your own numbers.

Gynger vs Founderpath Cost Calculator

Estimate the cost of a GyngerBill Financing draw side-by-side with Founderpath's Revenue Purchase Agreement (12mo, 7% starting flat fee) and Term Loan (24mo, 14% APR). Gynger does not publish a rate card — adjust the APR slider to your actual quote.

Gynger Inputs

Models Bill Financing / Virtual Card as amortizing monthly debt at a user-chosen APR over 3–12 months (Gynger's published term range). Gynger does not publish a rate card — set the APR to your actual quote.

Software Purchase / Bill Amount ($)

18%

12 months

Side-by-side Cost Comparison

Founderpath funds the company directly, so the same cash that pays the Gynger-financed vendor bill also covers payroll, headcount, or growth spend — and the FP RPA on a 12-month term beats Gynger on total cost at typical B2B BNPL APRs. The FP Term Loan stretches to 24 months for lower monthly cash burden.

Gynger (18% APR over 12mo)

$220,032

$20,032

$18,336/mo

Founderpath RPA (12mo, 7%/yr flat fee — cash to pay vendor)

$214,000

$14,000

$17,833/mo

Founderpath Term Loan (24mo, 14% APR — fixed monthly)

$230,462

$30,462

$9,603/mo

Fixed monthly

$6,032

in total cost on the same 12-month payback — and the FP Term Loan stretches to 24 months for an even lower monthly cash burdenGynger cost is modeled as amortizing monthly debt at a user-chosen APR over a 3–12 month term (per gynger.io/faqs). The APR slider is anchored to a typical B2B BNPL / virtual-card band consistent with Gynger's “lower APR than traditional credit cards” marketing language — this is an estimate, not a Gyngerdisclosure. Founderpath RPA modeled at 7% per year scaling with term; Founderpath Term Loan assumes a 14% APR — Founderpath's actual published starting rate, with no origination fee. Actual terms may vary.

Disclaimer: This calculator is for illustrative and educational purposes only. It does not represent an actual Gynger offer, quote, or financing term. All figures are hypothetical estimates based on publicly available information and user-provided inputs. Actual Gynger terms may differ significantly. Founderpath is not affiliated with Gynger and makes no representations about Gynger's current pricing or terms. Consult directly with any financing provider before making decisions.

Gynger Reviews (2026)

As of May 2026, Gynger does not maintain a profile on Trustpilot, G2, or Capterra and has no aggregated independent customer reviews. The only public testimonials live on gynger.io/customer-stories and are first-party — curated quotes plus aggregated outcome metrics, not independent reviews. Named customers include Lovd (refurbished tech), Harbinger (electric vehicles), CRS, Cylera (cybersecurity), Therapy iQ, Fillogic, Driveway, and HPE (which uses Gynger Pay as a vendor).

The customer-story aggregates include “50% growth” (CRS), “95% deal close rate” (Therapy iQ), “35% revenue increase” (Fillogic), and “15% software-spend reduction” (Driveway). These are Gynger-published claims; no independent verification is available.

By comparison, Founderpath maintains a 4.9 / 5 rating across 100+ verified Trustpilot reviews from SaaS founders. Reviews are searchable on Founderpath's Trustpilot page.

What Founders Say About Founderpath

David Tabachnikov

Founder of ScholarshipOwl

After Trying All the RBF Platforms, Founderpath Had the Best Terms

“After trying all the RBF platforms out there, we found FounderPath to be the best one to work with, having the best terms, and also giving us added value that nobody else could. FounderPath also worked with us to help us resolve our unique situation, and make our payment more predictable and flexible. With FounderPath, it's not just the money — it's being part of a financial support network.”

Jacob Wright

Founder of Dabble

Longer terms than others, & a personal touch

“Founderpath has been the best experience. You aren't just dealing with a sales rep who then hands you off to someone else. Founderpath has a more personal touch. They also have longer and more flexible terms, allowing you to pay off early if needed without penalty like the others. Overall, a great experience.”

Gynger vs Founderpath: Full Comparison

Based on Gynger's public website materials (gynger.io homepage, FAQ, buyer page, product page, customer-stories page), Series A and seed press coverage (Fintech Global, Built In NYC, Fintech Futures), TechCrunch on the revenue model, and industry-standard B2B BNPL contract provisions.

Feature | Gynger | Founderpath RPA | Founderpath Term Loan |

|---|---|---|---|

Who gets the capital | The vendor — Gynger pays the buyer's software bill upfront; the buyer never sees the cash | The SaaS company directly — cash on the balance sheet, usable for any expense including vendor bills, payroll, growth | The SaaS company directly — cash on the balance sheet, fixed monthly amortization |

Legal structure | B2B BNPL — buyer loan / receivables purchase against a financed invoice (Customer / Loan Agreement is not public) | Purchase of future receivables (not a loan) | Senior secured term loan |

Repayment type | Fixed monthly amortizing payments over chosen term (or net 30/60/90 balloon) | Fixed daily or weekly deductions on a set schedule | Fixed monthly payments |

Pricing model | Not publicly disclosed — TechCrunch (June 2024): interest + loan origination fees + card-program interchange + vendor service fees. Marketing language only ("low APR", "lower fees than factoring") | From a 7% flat discount fee scaling per year — published directly on the Founderpath product page | From 14% APR, fixed monthly, save on interest by repaying early |

Maximum term | Two structures (per gynger.io/faqs): 3, 6, 9, or 12-month amortizing monthly payments; OR net 30 / 60 / 90 single-balloon trade-term repayment (one lump sum at end of period) | Up to 36 months | Up to 48 months (4× Gynger maximum amortizing term) |

What it funds | A single technology vendor bill — SaaS subscriptions, cloud / GPU compute, IT spend | Any business expense — payroll, growth, runway, software, M&A | Any business expense — payroll, growth, runway, software, M&A |

Minimum revenue | Not publicly disclosed; Gynger markets to companies from "seed-stage startups to enterprise" | $100K annual revenue | $3M ARR |

Warrants or equity | No per gynger.io/about-us marketing ("without requiring the warrants…that other lenders demand") | No warrants, no equity, no board seats | No warrants, no equity, no board seats |

Personal guarantee | No per gynger.io/about-us: "without requiring the warrants, fees, commitments, and personal guarantees that other lenders demand." Confirm in the in-app Loan Agreement at draw time | No | No |

Public Terms of Service / sample agreement | No public Terms of Service, Privacy Policy, or sample Loan Agreement on gynger.io as of May 2026 — agreement is in-app at draw time | Standard Customer Agreement reviewed at term-sheet stage | Standard Customer Agreement reviewed at term-sheet stage |

Collateral * | Industry-standard B2B BNPL: UCC-1 on the financed receivable; broader covenants depend on private Loan Agreement | UCC-1 first position on future receivables and operating bank account | UCC-1 first position on all business assets |

Origination fee | In tension: gynger.io/about-us markets "without requiring the warrants, fees, commitments, and personal guarantees that other lenders demand"; TechCrunch (June 2024) confirms loan origination fees as part of revenue model — amount not disclosed | None | None |

Early repayment | Not publicly disclosed; depends on the in-app Loan Agreement | Full discount fee applies (no savings on early exit) | Save on interest by repaying early — no prepay penalty |

Funding speed | Up to 24 hours for approval; vendor paid the next business day (per gynger.io/faqs) | Under 24 hours | Under 24 hours |

Geography | US-only based on publicly available information (US HQ, US-centric vendors and customers, Codat / Plaid US integrations) | Global | Global |

Reviews on Trustpilot / G2 / Capterra | No profile or aggregated reviews on Trustpilot, G2, or Capterra as of May 2026 | 4.9 / 5 across 100+ verified Trustpilot reviews | 4.9 / 5 across 100+ verified Trustpilot reviews |

Best fit | Buyers who want to spread a single tech vendor bill — or vendors who want an embedded BNPL widget at checkout | SaaS founders worldwide who want working capital + apples-to-apples MCA structure | SaaS founders worldwide who want working capital + the longest fixed-monthly term |

Public Sources

- Gynger marketing pages (linked inline above): gynger.io homepage, /faqs, /buyers, /product, /capital-ap, /customer-stories, /about-us, and /resources/blog/gynger-partners-with-soluna. Confirms product lineup (Bill Financing, Reimbursement, Virtual Card, AR Financing, Gynger Pay), term options (net 30/60/90; 3, 6, 9, 12-month payments), approval timing (~24 hours), supported vendors (Snowflake, Salesforce, AWS, Google Cloud, Cisco, Datadog, Okta, Oracle, HubSpot, Adobe, CrowdStrike, Braze, Amplitude, Lambda Labs, VMware, Dell, CDW), and the Soluna direct-partner integration. HPE quoted on /customer-stories as a Gynger Pay vendor.

- “Embedded financing pioneer Gynger raises $20M in Series A round,” Fintech Global, June 21, 2024 — Series A $20M led by PayPal Ventures with Gradient Ventures, Velvet Sea Ventures, BAG Ventures, Deciens Capital participating; $100M debt facility from Community Investment Management (linked inline above).

- “Gynger lands $21.7m as it arises from stealth,” Fintech Global, Dec 28, 2022 — Seed $11.7M equity led by Upper90 and Vine Ventures, plus a $10M debt facility from undisclosed lenders; Gradient Ventures, Deciens Capital, Quiet Capital participating (linked inline above).

- “Gynger raises $20M Series A,” Built In NYC, June 21, 2024 — confirms employee count and growth statistics at the Series A milestone (linked inline above).

- “PayPal Ventures leads $20M round into Gynger, which helps companies finance their tech purchases,” TechCrunch, June 20, 2024 — describes revenue model: “charges interest on its loans and also makes money from buyers on loan origination fees, as well as through interchange fees from its card program… and also generates revenue from vendors via service fees and plans to generate revenue from SaaS/platform fees.” Indexed via techcrunch.com (article URL has been observed to return 404 from non-browser requests; content is browser-accessible and mirrored on Built In NYC).

- “US start-up Gynger completes $20m Series A and lands $100m debt facility,” Fintech Futures, June 21, 2024 — corroborates Series A + debt facility details. fintechfutures.com URL returns 403 to non-browser requests; works in standard browsers.

- GTMnow Podcast Episode 109, “Building Braze From Zero to IPO — Mark Ghermezian,” 2024 — gtmnow.com — Ghermezian discusses raising Gynger's Series A in a post-Braze-IPO market.

- Gynger LinkedIn company page — linkedin.com/company/gynger — confirms NYC HQ and the “11–50 employees” band.

- Crunchbase Gynger profile — crunchbase.com/organization/gynger — independent corroboration of funding rounds and investor list. Returns 403 to non-browser requests; works in standard browsers.

- Trustpilot, G2, and Capterra searches for “Gynger” / “gynger.io” — no company profile or aggregated reviews exist as of May 2026 (absence confirmed via direct query).

Industry-Standard Provisions

* Rows marked with an asterisk reflect provisions standard in B2B BNPL / receivables-purchase lender contracts (UCC-1 security on the financed receivable, default and acceleration mechanics, origination-fee disclosure timing). These provisions are not individually confirmed in Gynger's public marketing materials — Gynger does not publish a Terms of Service, Privacy Policy, or sample Loan Agreement on gynger.io as of May 2026; the financing-specific Loan Agreement is signed inside the Gynger app at the time of each draw. Specific clauses may vary by deal. We recommend requesting and reviewing the full Loan Agreement before drawing on any Gynger facility. If any information on this page is inaccurate, contact us at hello@founderpath.com and we will promptly review and update.

Gynger Overview: Pricing, Timeline, Company Facts

At-a-glance reference card on Gynger's product structure, eligibility, and corporate facts — sourced to gynger.io (homepage, /faqs, /buyers, /product, /capital-ap, /customer-stories), Fintech Global, Built In NYC, Fintech Futures, TechCrunch, and the GTMnow podcast.

Pricing & Products

- Bill Financing

- Gynger pays vendor upfront; buyer repays Gynger over 3, 6, 9, or 12 months (or net 30/60/90 balloon)

- Reimbursement

- Retroactively finance an already-paid software bill

- Virtual Card

- Gynger-issued card for recurring tech spend; “lower APR than traditional credit cards”

- AR Financing

- Vendor-side advance on outstanding customer invoices

- Gynger Pay

- Embedded vendor-checkout BNPL widget; vendor gets paid upfront, buyer pays Gynger

- Cloud / HPC

- Lambda Labs supported on homepage vendor list; direct partnership with Soluna (renewables-powered HPC) per gynger.io blog

- Rate

- Not publicly disclosed; per TechCrunch (Jun 2024): interest + loan origination + card interchange + vendor service fees

- Max Term

- 12 months on the amortizing option (3/6/9/12mo monthly schedule); 90 days on the single-balloon option (net 30/60/90 trade terms)

Timeline & Requirements

- Min Revenue

- Not publicly disclosed; Gynger markets to companies from “seed-stage startups to enterprise”

- Integrations

- Codat (accounting), Plaid (bank linking)

- Geography

- US-only per all publicly named customers, vendors, and integration partners

- Approval

- Pre-qual in minutes; full approval as fast as 24 hours

- Funding Speed

- Vendor paid the next business day after approval

- Covenants *

- Public Terms of Service / sample Loan Agreement not published; in-app agreement at draw time

Company Facts

- Legal Name

- Gynger, Inc.

- Founded

- 2021; emerged from stealth December 2022

- Headquarters

- 157 W 18th Street, Floor 5, New York, NY 10011

- Founder

- Mark Ghermezian, CEO — also co-founder and founding CEO of Braze (NASDAQ: BRZE); GP at MXV Capital (mxv.vc)

- Employees

- 11–50 employee band per LinkedIn (2026); about-us page profiles ~35 team members

- Customers

- Lovd, Harbinger, CRS, Cylera, Therapy iQ, Fillogic, Driveway, HPE (vendor / Gynger Pay)

- Backers

- PayPal Ventures (Series A lead), Gradient Ventures (Google), Velvet Sea Ventures, BAG Ventures, Deciens Capital, Upper90, Vine Ventures (Seed leads), Quiet Capital; CIM debt facility

Gynger Funding, Valuation & Investors

Gynger has raised approximately $31.7M in disclosed equity across a December 2022 seed and a June 2024 Series A, plus a $110M committed debt-facility stack ($10M at seed from undisclosed lenders, $100M at Series A from Community Investment Management). No post-money valuation has been publicly disclosed for either round. No 2025 or 2026 follow-on round has been announced as of May 2026.

Round / Fund | Amount | Date | Notes |

|---|---|---|---|

Seed (equity) | $11.7M | Dec 2022 | Co-led by Upper90 and Vine Ventures; Gradient, Deciens, Quiet Capital participating |

Seed (debt) | $10M | Dec 2022 | Debt facility from undisclosed lenders |

Series A (equity) | $20M | Jun 2024 | Led by PayPal Ventures; Gradient, Velvet Sea, BAG Ventures, Deciens participating |

Series A (debt facility) | Up to $100M | Jun 2024 | From Community Investment Management (CIM) |

Gynger's capital structure mirrors a typical B2B-lending fintech: a thin equity sleeve plus a much larger debt-facility backstop to fund the loan book. The CIM facility is the lending capital; the equity is for the platform / engineering / sales build. Gynger has not publicly disclosed a post-money valuation for either round, and revenue / margin metrics are not published by the privately held company.

By comparison, Founderpath operates a SaaS-recurring underwriting thesis and funds founders globally. Founderpath has deployed over $271M in non-dilutive capital to 740+ SaaS founders to date — capital that goes to the company directly, not to a single vendor invoice. The differentiator for founders evaluating Gyngervs Founderpath isn't legitimacy — both are well-capitalized operators — it's structural: vendor-financing vs working-capital, locked-purpose cash vs general-purpose cash, undisclosed APR vs published 7% / 14%.

Founderpath vs Gynger: Which is Right for Your Business?

Founderpath and Gynger solve adjacent — not overlapping — problems. Gyngerpays a buyer's software vendor upfront and spreads the bill over 3–12 months; the cash never touches the buyer's bank account. Founderpath funds the SaaS company directly, on the company balance sheet, for any use — vendor bills, payroll, growth, runway, M&A. If the founder's only goal is to extend a single vendor's payment terms, Gynger is the cleaner instrument. If the founder wants capital flexibility across multiple uses and a longer payback window than 12 months, Founderpath is the better fit.

Founderpath offers three capital products: a Merchant Cash Advance (MCA) for seasonal businesses (% of monthly sales repayment); the Revenue Purchase Agreement (RPA) for recurring-revenue founders who want fixed daily or weekly debits at a 7% starting flat fee scaling per year (terms up to 36 months); and a Term Loan for founders who prefer fixed monthly payments (14% APR starting, terms up to 48 months — four times Gynger's maximum). All three wire funds in under 24 hours, with no personal guarantee, no origination fee, and no in-app contract surprise — the Customer Agreement is shared at term-sheet stage.

Gynger's sweet spot is a SaaS founder or finance team that wants to defer a single big software bill (Snowflake, Salesforce, AWS, a multi-year contract) by 3–12 months without renegotiating the vendor relationship. Founderpath's sweet spot is a SaaS founder who needs working capital — to pay vendor bills AND fund payroll, growth, or runway from the same advance, on a longer payback window than Gynger's 12-month maximum. See the full Gynger vs Founderpath comparison table above for a row-by-row breakdown.

Founderpath is the Fastest Growing Gynger Alternative

Frequently Asked Questions About Gynger

Pros: pre-qualification in minutes and approval in 24 hours, no warrants, no equity, no traditional personal guarantee, multiple product flavors (Bill Financing, Reimbursement Capital, Virtual Card, AR Financing, Gynger Pay), and a credible founding team.

Cons: no published rate card, 12-month maximum amortizing term (shorter than most SaaS-specialist lenders), only finances technology vendor invoices (not general working capital), no public review footprint, undisclosed origination fee per TechCrunch, US-only, and lender contracts not publicly available before draw.

This comparison was written by the Founderpath team — direct operators with $271M deployed to 740+ SaaS and ecommerce founders — based on Gynger's publicly available information (gynger.io homepage, /faqs, /buyers, /product, /capital-ap, /customer-stories) and independent third-party reporting from Fintech Global, Built In NYC, Fintech Futures, TechCrunch, and the GTMnow podcast. Public sources are cited with links throughout and below the comparison table.

Disclaimer: All figures in the comparison table are based on publicly available information and independent third-party sources. Gynger does not publish a standard rate card, Terms of Service, Privacy Policy, or sample Loan Agreement on its public site as of May 2026 — actual fees, covenant terms, and contract provisions vary by deal and are revealed in the in-app Loan Agreement at draw time. We recommend that all founders request and carefully review the complete Loan Agreement before drawing on any Gynger facility. If you believe any information on this page is inaccurate, please contact us at hello@founderpath.com and we will promptly review and update.

Get a Founderpath Offer in Under 24 Hours

Skip the per-invoice BNPL. Connect your integrations, get a real offer with no commitment, and see your monthly payment before you decide. Cash on the balance sheet — usable for vendor bills, payroll, growth, and runway from one facility, with a payback window up to 48 months.

Get Your OfferKeep comparing

More Founderpath comparisons

Tired of one-at-a-time comparisons?

Enter your amount and term once — see all 24+ lenders ranked by total cost and effective APR.

Founderpath vs Capchase

6–12 mo·ARR advance (flat fee)PG: VariesARR-based advances with shorter 6–12 month payback; Founderpath offers up to 48 months.

Read comparison →

Founderpath vs Clearco

6–12 mo·Merchant cash advanceNo PG50% daily revenue sweep on Cash Advance, 5–8% flat Invoice Funding fees; no early-payoff discount.

Read comparison →

Founderpath vs Pipe

6–12 mo·MCA via partnersPG: VariesRecurring-revenue marketplace pivoted to merchant cash advance via Stripe and Shopify partners.

Read comparison →

Founderpath vs Wayflyer

3–9 mo·Merchant cash advancePG: VariesEcommerce-focused MCA with daily revenue percentages; Founderpath funds SaaS at lower disclosed rates.

Read comparison →

Founderpath vs Lighter Capital

3–5 yr·Revenue-based financingPG: VariesRevenue-based financing with monthly variable payments tied to top-line revenue.

Read comparison →

Founderpath vs SaaS Capital

Up to 5 yr·Credit facility (covenants, warrants)PG: YesCommitted credit facility for SaaS companies above $5M ARR with covenants and warrants.

Read comparison →

© 2026 Founderpath, Inc. All Rights Reserved.